Bizarre ads for TransferWise, a P2P money-transfer system, have cropped up overnight in NYC’s subways. I had many questions: who is this guy? Why his face? What is he selling me? Turns out the more you try to learn about TransferWise, the sketchier the whole thing becomes.

On the surface, TransferWise looks like any other startup in the fast-growing field of monetary transactions. Founded by Taavet Hinrikus, “Skype’s first employee,” and his friend Kristo Käärmann, the company is “Estonian made” and based in the UK. TransferWise’s mission is to circumnavigate the fees banks charge to transfer money from one country to another, offering a P2P exchange via algorithm instead. Peer-to-peer transactions are TransferWise’s bread and butter.

I’ll let The Economist explain:

If someone in Britain, say, wants to transfer money to his relative in Spain, he will put the cash in Transferwise’s British account. The algorithm then spots someone in Spain who wants to make a transfer in the other direction, and who deposits funds in the firm’s Spanish account. Rather than crossing borders to reach its destination, money can simply be paid out of the relevant national account.

TranferWise has an innovative model that many living and working abroad will appreciate. Banks charge outrageous fees for the privilege of moving your hard-earned cash out of the country — often between 3-6 per cent — and that sucks. But banks are generally highly insured and do not set off all of your “sketchy internet” alarm bells when you Google them.

I’m not claiming that TransferWise is a completely shady operation. The company has several years on the start-up radar, backing from the likes of Peter Thiel’s Valar Ventures and PayPal cofounder Max Levchin, winningly photogenic co-founders, and an office in London.

They have been written up by outlets like the Economist, Wired.co.uk, and Gigaom (RIP). But when money is involved and the rules of banking are being broken, things start to look a little fuzzy. The Economist closes its coverage with a warning about money laundering and asymmetric demand for exchanges:

Critics point to the risk of money-laundering. TransferWise retorts that it is subject to the same “know your customer” rules as any commercial bank. A bigger problem is scaling up in countries that have fewer immigrants than émigrés. The demand for converting Indian rupees, say, into pounds may be less than the demand the other way. That means you still need a bank to stand in the middle of a transaction. Not “bye-bye”, then, but a possible black eye.

So there are a lot of potential problems here, especially for developing countries whose currencies aren’t as widely desired. The UniBul Credit Card blog struggled with the same issue inherent to TransferWise’s set-up:

[Y]ou can immediately see the problem in such a scheme: it can only work in the manner described above for as long as there is a balance in the flow of money between each pair of countries served by the service provider. The problem is that in the real world such a balance does not exist.

Let’s dig deeper.

There is zero doubt that TransferWise has aggressively gamed its SEO to thwart its critics, especially when you go searching for “TransferWise scam.” One of the first sites that pops up, “transferwisereview.com,” uses the same language seen in the company’s marketing elsewhere to tout how “revolutionary” TransferWise is. It’s there to allay any of your fears:

It’s very difficult to find any negative feedback. There are just few minor complaints:

- It’s not possible to pay with debit card for transfers of over £2000

- They didn’t replay to one of my emails

- Transfers could be faster (less than one day)

I wonder why it is so difficult to find any negative feedback. Said no one ever.

The “review” site is set up to look sort of like an independent blog reporting on the company, and it raises every hackle that I have. If the company has nothing to hide or fear, why are they literally covering themselves? Many of the “trusted reviews” found on other sites also read like they were written by a copywriter with a gun to their head.

Look, TransferWise isn’t evil. Anything that saves humankind a few bucks snatched back from the maw of big banking gets my vote. If I were living abroad, I’d probably use it. But I’d have serious reservations about the longterm viability of the scheme — especially since a little searching shows the company to be so keen to project positivity and bury possible criticism. Something just seems off.

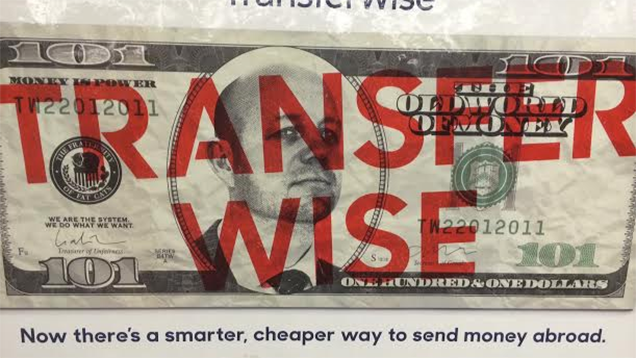

A few years ago, TransferWise wasn’t approved for US transactions, but times have changed. The company appears to be aiming for the American constituency least concerned with proper regulation — the real message when you examine the New York subway ads up close. The ad thumbs its nose at big banking, grabbing for the growing Libertarian market that loves crypto-currency and hates government regulations: “WE ARE THE SYSTEM. WE DO WHAT WE WANT,” the “$US101 dollar bill” proclaims, under a crest that reads “THE FRATERNITY OF FAT CATS,” signed by “the Treasurer of unfairness.”

But to the majority of New Yorkers, the ad catches the eye by proffering an unknown face and a hefty promise. Is this an attempt, as Venmo somewhat managed with its Lucas campaign, to drive interest through sheer ubiquitous befuddlement?

Perhaps it’s working, since I snapped a picture of the ad at once, and other Gizmodo staffers had noticed it. Does this ad inspire you to let TransferWise handle your money? Are you ready to reject “the secretary of Greed” and “the old world of money”? Why is a balding white guy with beard scruff the face of TransferWise? Considering the desired demographic, did I just answer my own question?