As the Silk Road came tumbling down yesterday, and its signature currency — Bitcoin — has been pushed into the spotlight again. Will Bitcoin survive? Should it survive? Should people keep using it if it does? We’re here to talk it out.

The fact that all this trading was taking place over the internet and with an entirely virtual currency makes this a particularly sticky issue to grapple with, but for better or worse, digital currency is already here. The percentage of people who carry actual cash is dropping as alternatives like credit cards, Square, online banking, and NFC continue invading every corner of the market. But Bitcoin is a different beast.

The Good

For all that Silk Road craziness, Bitcoin has its upsides, depending on who you talk to, anyway.

No one’s in charge

One of Bitcoin’s biggest drawbacks is also its biggest strength: a lack of a regulating body. Whether that’s good or bad is a matter of who you ask.

Bitcoin is complicated, but the system works a little something like this. Each Bitcoin maintains a single, public record of past and current ownership. Then, every eight minutes, a network of verifiers checks the public Bitcoin ledger against their own to make sure that they line up, at which point they’re rewarded with newly created Bitcoins for their hard work. And that, boys and girls, is how Bitcoins are mined (and regulated). It’s a weird system, but it’s not beholden to any big man with a cigar. It just sort of does its thing. It’s free in a unique sort of way other currencies aren’t.

Decentralisation

It can be kind of hard to wrap your mind around a currency with no inherent value, but the US dollar falls under that very same description. Ever since Richard Nixon axed the gold standard in 1971, US currency has had nothing physical to back it up. From the US Treasury to Bank of America’s databases, our entire currency system is resting on one big, elaborate web of trust. The United States government is pretty good for a third-party regulator, but nothing is without its flaws.

This is the hole that Bitcoin attempts to fill. Instead of relying on some higher authority the Bitcoin market depends on cold, hard maths — an algorithm fuelled by a decentralised network and open-sourced code that is always available for public viewing. Theoretically, were the US economy to suddenly come crashing down (be it because of bank bailouts, derivative trading, or war), the Bitcoin could continue on nearly unencumbered. In other words, Bitcoin could be a potential buffer against a total global financial system collapse. That is, if it’s not busy crashing for its own reasons. Nothing is perfect, but being separate can be good.

Freedom

Another benefit of this lack of central control is that the government can’t block you from giving out Bitcoins. In 2010, the US government sought to silence Wikileaks by cutting off its money supply. Both banks and credit card companies were forbidden from transferring any incoming donations to the site. No matter how you feel about Wikileaks, it’s hard to deny there’s some troubling implications there.

As soon as the United States started enacting its financial holds, Wikileaks began suggesting that its users donate using Bitcoin — something the government wouldn’t be able to control or stop. Granted, this sense of lawlessness and anonymity can be used for some shady practices, but its this kind of freedom makes Bitcoin powerful for folks who are supporting something unpopular, whether it’s Freedom or a local drug dealer.

The Bad

Of course, there’s a reason anarchy doesn’t work in practice. Without any sort of central regulation, there’s no framework for control. People can leverage Bitcoin for their own unsavory purposes pretty easily. The Silk Road was bursting with those folks.

Anonymity for Evil

Although each Bitcoin is stamped with a transaction history, the signatures are of a shadow people. No identifying information is buried within those numbers, and its nearly impossible to track someone down based on a trail of Bitcoins alone. Free from government control and tracking, someone with ill intent can all too easily acquire not just drugs but weapons or whatever else with little fear of being tracked down. Of course good old-fashioned cash can be pretty untraceable too, but you can’t pay with physical dollars over the internet.

A Dependence on the Undependable

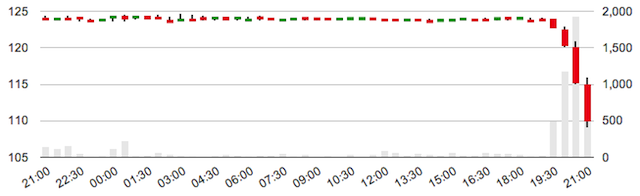

Bitcoin might be free from the fluctuations of the US economy, but that doesn’t mean it’s invincible. Just look at today’s Bitcoin price chart.

This USD-equivalency chart is shocking for its dramatic drop, yes, but also for what it tells us about the present nature of Bitcoin itself. This virtual currency that’s often held up as a failsafe in the event of a conventional currency apocalypse isn’t rock-solid. Far from it. Between a digital drug bust and a healthy dose of resulting investment fear, the Bitcoin took a nose-dive today. And not for the first time. But it hasn’t died for good yet.

So in terms of should we or shouldn’t we, there really is no easy answer. Yes, Bitcoin has its downsides, but it’d be exceedingly hard to regulate. And probably harder to stop.

Besides, it may burn out on its own. Past competing currencies haven’t lasted done too well in the past — just look at the Liberty Dollar. Its devotees enjoyed about eight years of a private, non-federally-backed currency before the United States went after its creator for counterfeiting. Bitcoin, of course, is much more difficult to pin down. It’s virtual, and its servers aren’t technically on US soil. Regardless, with today’s events, it seems like Bitcoin could be on its way to being outlawed, whether it should be or not.